Why do you sometimes receive less from your life insurance than expected? It is not an out-and-out savings product, but also covers the mortality risk.

How is the premium paid in used?

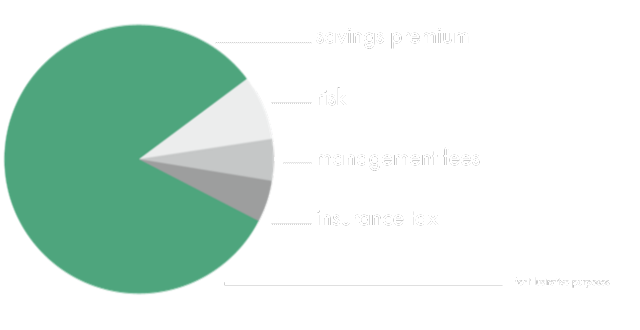

The contributions you make are not fully saved, but instead are assigned to different areas:

Classical life insurance

The insurance undertaking guarantees your a defined sum insured. Interest is paid on the savings premium for the agreed guaranteed interest rate. The guaranteed insurance benefit therefore corresponds to the proportion of premiums that are saved, plus interest as the guaranteed interest rate, less taxes, fees for concluding the contract, management fees and fees for risk. In addition to the guaranteed sum insured, you may also receive a participation in profits. This arises from the insurance company doing business using your savings premium, and investing for example in bonds, shares or real estate. This variable participation in profits depends on the insurer’s performance and how the capital markets perform, and cannot be guaranteed in advance.

Funds- or index-based life insurance

In the case of fund-linked life insurance plans your investment premium is invested in investment funds, whereas in the case of index-linked life insurance the premium is linked to the performance of a specific index or benchmark. When your contract expires, you do not receive a predetermined insurance benefits, but instead the current value of the fund units (or the index). The development of the value of the fund or index cannot be predicted, but is vulnerable to fluctuations and may even be negative.

Your amount is decreasing?

Why do you sometimes get less money back than you have paid in? One possible reason is that the fees, taxes and charges sometimes exceed the return.

Return:

classical life insurance primarily invests in fixed-income securities attracting a low rate of interest. In the case of funds and index-based life insurance the capital markets may perform unfavourably.

Costs:

commission due for concluding a contract, management and insurances fees reduce your credit balance.

Taxes and charges:

depending of the type of contract subsequent tax deductions may lower the pay-out.

Early redemption …

… often comes with financial disadvantages:

- the surrender value is often significant lower that the contributions that have been paid in. Especially during the first years there are a lot of charges deducted, resulting in a disappointing pay-out.

- Guarantees usually only apply at the end of the term: if you choose to redeem beforehand, you are likely to lose capital protection cover.

- The surrender value may be impacted by deductions for cancellations.

Alternative to cancelling your insurance:

Instead of cancelling your insurance, it might make sense to instead switch to a contribution-free approach – the contract continues to exist, without requiring you to make further payments.

Our tip

Comparisons keep you safe!

The insurance company is required to provide you with standardised key information documents for classical, funds-based and index-based life insurance products. They contain important information about the type, risk, costs as well as potential profits and losses for the insurance.

Other editions:

28 Health Insurance

24 Low risk investing

26 Poverty in old age

Find out more:

A-Z of Finance: www.fma.gv.at > A-Z of Finance

Instagram: @redenwiruebergeld

Podcast: listen here!